I've come up with an approach that might appeal to viewers of the Pulsenomics quarterly survey of home price expectations or that might even impact forecasts in the future.

I've touted the quarterly survey for 10+ years (when I first became a participant) as great way for readers to stay abreast of the forecasts of >100 experts in housing finance/economics. However, it's bothered me that some participants have strong outlier views (both bullish and bearish) but that none have not been responsive to my invitations/prompts to back those views with trades on the CME Case Shiller home price index futures. Further many of their clients (as many forecasters are in consulting or education) might be looking for a way to embrace or reject such calls.

As a for instance, here's a summary of the most recent survey, with my inputs (yellow), and the year-end values for 2026 bolded in red. (I included mine so that you can see where I come up with my numbers). Note that the median is 7.51% but that the standard deviation is >4 points! Such differences of opinion would seem to present great opportunities for those that disagree to trade/financially express such views.

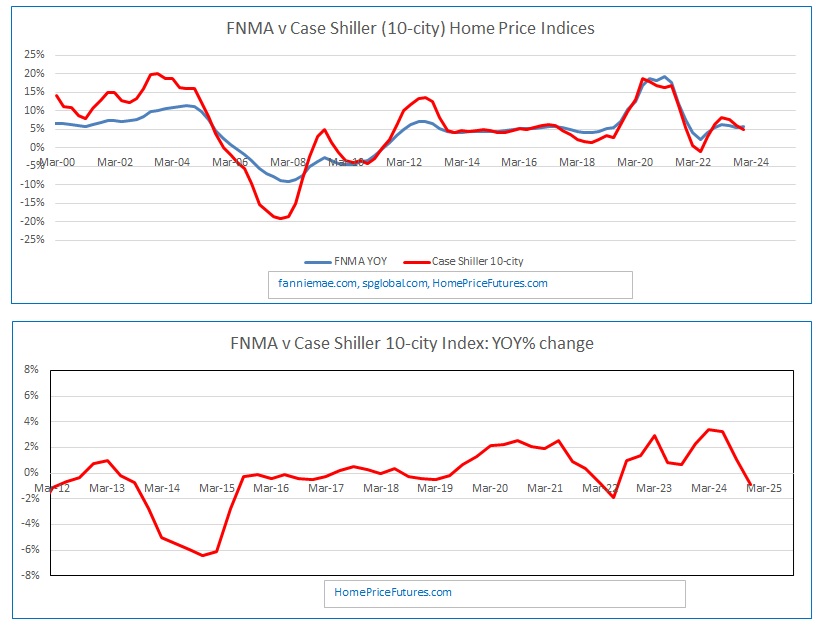

Since the (relatively new) reference index for this survey is the quarterly Fannie Mae home price index^1 , I'd argue that the Case Shiller index released in Feb 2027 (that measures activity during the last quarter of 2026) might be a close match for changes in the Fannie Mae index (at least as to quarterly measurement period) for year-end 2026. In fact, (as shown in the graph below) while the Case Shiller index (in red) has been more volatile (particularly during the Financial Crises) since 2015, the difference in year-on-year percentage changes between the indices have been highly correlated, have rarely exceeded 2%, and have tended to revert. The Fannie Mae index has modestly outperformed (See below).

Since the CME Feb 2027 HCI (or CUS index, depending on your trading platform) contract settles on the 2026 year-end numbers, I would argue that a large component of contract prices for that contract reflect expectations for where the Case Shiller (and by correlation) the Fannie Mae index) will be at year-end 2026.^2

But there's more. Using the Ratio Agreement framework that I've applied to other OTC situations (e.g. ^3), one can see that the ratio of the Fannie Mae/Case Shiller index (the black line on the left) has been relatively stable since 2013. (The current ratio is 0.9806 (equal to the Fannie Mae Q4 spot index of 343.73 divided by the Case Shiller Dec index -released in February -of 350.52). That the Fannie Mae index has modestly outperformed can be seen in the rising value of the ratio (which happens when the numerator goes up higher than the denominator.)

I'm showing indications on where I'd buy (yellow diamonds)/sell (green circles) the Fannie / Case Shiller Ratios for year-end 2025 and year-end 2026 index values. (Note that my quotes are consistent with continued outperformance of Fannie v Case Shiller).

Combining those ratios with a futures position in the CME Feb '26/ '27 10-city index contracts (See quotes in upper right) leads to indicative pricing for the Fannie Mae index for each year end.

So, my posted quotes on Fannie Mae for year-end 2026 are equivalent to +6.03% (bid) vs + +8.52% (ask). (This is how I use the CME futures to back into my Fannie Mae forecasts.) There were 83 respondents in the last survey who projected that Fannie Mae index for year-end 2026 would be either less than 6.03% or higher than 8.52%. Now, post the updates that have taken place in the market since the surveys were compiled in early March, if any of them (or their clients) want to financially express those views, the process of combining a Fannie /CS ratio Agreement with an outright position in the CME Case Shiller futures, allows them to do so.

Note that the CME contract addresses the vast majority of counterparty price risk. That is, while the Fannie Mae index is +81% since year-end 2016, the ratio between the Fannie Mae and Case Shiller index has only moved ~7%. More than 90% of the price move in the Fannie Mae index is explained by movements in the Case Shiller index. As such, if home prices rise or fall 15% parties to these agreements will get margin calls from the CME.) ^34

Further, since the contracts are updated continuously, one can observe changes in those contracts to infer updated market risk-clearing levels on the Fannie Mae index (rather than waiting for the next quarterly survey).

BTW - There's been plenty of mortgage-related and economic headlines since the Pulsenomics participants sent in their forecasts in late Feb/early March (e.g. tariffs, mortgage rates dancing with changes in the yield curve, stock market selloff destroying wealth). Surprisingly (see graph below) there has been little change in the benchmark HCI (10-city index) contract for Feb 2026. (Today April 15 that contract is quoted 362.0-364.0). I'd be curious to hear if any of the Pulsenomics participants have changed their forecasts.

I've only shown examples for year-end 2026 and 2027, but the concept would work the same for 2028-2029 (as there are CME expirations out to Feb 2030.)

I realize that combining two moving parts (a Ratio Agreement and a Futures contract) to create a single exposure can be challenging, even off-putting, but I don't know of another public market where one can lock in the majority of exposure to changes in the Fannie Mae home price index.

Feel free to contact me if you any question or trade ideas.

Thanks,

John

^1 See https://www.fanniemae.com/newsroom/fannie-mae-news/home-price-growth-reaccelerates-fourth-quarter for their most recent press release

^2 Now a qualifier, I've long written that CME contracts reflect levels where risk clears on a thinly traded contract, and may not reflect pure expectations.

^3 See https://www.homepricefutures.com/posts/adding-more-information-to-reformatting-hphf-ratio-agreement-template for a recent blog on Ratio Agreements.

^4 See FN 2 for a discussion on how counterparty risk is addressed in HPHF Ratio Agreements.

#homeprices #realestate, #broker #mortgage